This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This is the effect of Dopamine Banking, where finance meets emotions and entertainment, and every tap of your smartphone is engineered to delight and reward. Traditional banking often struggles to capture and maintain customer engagement. Traditional banking often struggles to capture and maintain customer engagement.

Traditionally, the banking industry has been slow to innovate. In this ProductTank London talk Megan Caywood, then Chief Platform Officer at Starling Bank, explains how the bank has challenged the status quo by introducing a current account that is entirely digital and tailored to the smartphone generation.

Radical shifts are taking place in the banking industry. As a result, the banking industry is indeed facing several challenges. Upgrading legacy banking systems in order to support innovations of today is also a challenge, however, with blockchain? digital transformation in traditional banking is possible.

How does customer onboarding in banking work? You will also learn the main challenges involved in the onboarding process in banking, best practices and explore the best onboarding software tools for the job. The process establishes the foundation for the bank-customer relationship. Why do you need it in the first place?

Banks have always relied on predictions to make their decisions. Today, banks realize that data science can significantly speed up these decisions with accurate and targeted predictive analytics. Today, banks realize that data science can significantly speed up these decisions with accurate and targeted predictive analytics.

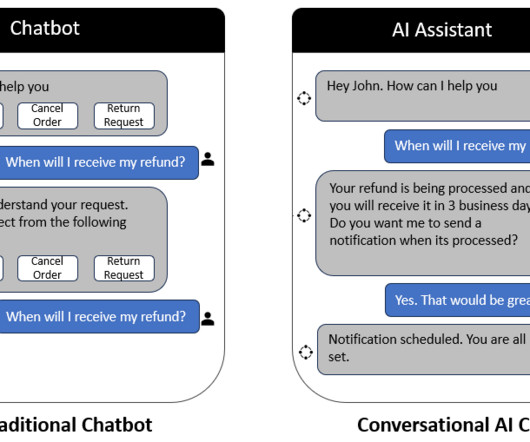

Banking on Conversation: The Future of User Experience with Conversational UI Image created by the author using Bluewillow AI How many times do we all log in to our banking app and struggle to find information? This is precisely where Conversational UI banking is revolutionizing the retail banking industry.

From Banking to Tech: Lessons from her time at JP Morgan and pivoting into entrepreneurship. If you’re struggling with perfectionism in your product role, this episode offers key lessons in letting go and focusing on impact. Learning to Build: How coding bootcamps helped Maya develop problem-solving skills.

“To date, none of the banks in the BVI have said that my businesses were feasible to support any of them,” said Rochelle Lawrence, a local entrepreneur, who shared her story at the BVI Business…

For example, a bank may receive frequent in-app feedback about navigation issues in its mobile banking app. If many customers report difficulty with account settings, the bank can prioritize improvements to the user interface (UI).

AI has the power to transform countless industries — including the healthcare, banking, insurance, and public service sectors, to name just a few — by introducing new efficiencies and revealing new opportunities for companies to solve problems.

In the world of digital banking, creating an app that truly resonates with users is no small feat. That’s why we’re thrilled to celebrate our partner Alkami Technology’s recent win as “Best Banking App” in Tearsheet’s 2024 Big Bank Theory Awards.

Subcategories for Finance Apps: Fintech, Banking, Insurance. “Why do people like mobile banking? Banking (banks and credit unions), and Insurance (auto, home, life, renters, pets, etc.). Response rates were phenomenal, with 94% for Fintech, a whopping 98% for Banking, and a high 97% for Insurance (91% overall).

Previously he worked for two of the UK’s largest banks, RBS/NatWest and Barclays, on their Mobile Banking apps, and most recently for The Sun, one of the world’s largest online publishing brands, where he was responsible for their news apps. The Best Visionary Product.

Banks have always relied on predictions to make their decisions. Today, banks realize that data science can significantly speed up these decisions with accurate and targeted predictive analytics. Today, banks realize that data science can significantly speed up these decisions with accurate and targeted predictive analytics.

I was at dinner last night and this came up where a number of consultants were sharing about how we work with teams and one was a bank and they said they weren’t allowed to talk to their customers. We were like, yes, but everybody you know banks. It turns out the way you bank is probably really similar to the way that I bank.

While we saw DAU (daily active users) stay pretty consistent for traditional banking apps since the pandemic hit, it spiked for budgeting apps and other mobile-first brands. Historically, the banking experience has never been one to write home about. Let’s unpack that a bit more. And right now, human connection is everything.

Many organisations that have adopted Scrum like banks, retailers, and media companies traditionally don’t have a product management group and hence no product mangers. Secondly, Scrum has been applied outside the realm of product development and commercial software products.

Unlike the banks, we display our fee upfront and deduct it before currency conversion. TransferWise was formed in 2011 out of frustration with the expense of sending money overseas. We use the mid-market exchange provided by Reuters with no mark-up, so there are no nasty surprises for customers. We’re happy to boast that the service [.].

But many banking and financial services companies are falling behind on their retail, media, and technology counterparts when it comes to product personalization. Rapid technological advances & high consumer expectations have changed the game for financial institution products. Listen up, Product Managers!

Another challenge comes with the unique loyalty customers feel towards their financial institutions and banks. Inefficient customer service is one of the main reasons why customers leave their banks or financial tools. Bank offers Face ID and Wells Fargo has 128-bit encryption to mask sensitive information.

I went on being called a Business Analyst as I worked at banks and other financial services companies. I was doing a workshop for a very large bank when one of the attendees chimed in. I wasn’t called a Product Manager until I bailed out of that and landed in a startup. I rarely thought about it after that.

Imagine you’re building accounting software, and you’ve just launched a new feature, automated bank reconciliation. In your session replays, it hides sensitive data like passwords, bank details, and addresses. The thing is, not all of them are relevant in a particular context. The best part?

By understanding the latest threats and their solutions, you can come out of this crisis stronger than ever--without breaking the bank. As technology leaders, it's time to rethink some of your product security strategy. We are excited to be joined by a CTO who is an expert in pragmatic choices around security.

Innovation-thinking banks and fintech startups use natural language processing to augment intelligent chatbots into the customer experience. Banks can use NLP-powered chatbots to provide 24/7 customer assistance and personalized insights based on real-time financial data analysis.

Another example involved a bank that had strong company policies that meant their product teams were not allowed to talk to customers. It just mattered if they banked somewhere. Fortunately, the team knew plenty of people who had bank accounts at other institutions.

In our digital world, it has never been easier for customers to switch banks, wealth and investment managers, or financial technologies. 40% of banking customers are willing to leave their provider for a better digital experience alone! The first step to meeting these expectations is assessing your current experience.

After working at Northwestern University, I became a consultant and was responsible for servicing one of the largest banking institutions in the nation. Due to recent changes to the bank’s business goals, 20,000 accounts were deemed unserviceable and I was given the task to remove 20,000 accounts from the system.

If you've ever called a bank, cable company, or organization that thinks it's "too big to fail", you've probably run the customer service gauntlet: you start off with a seemingly simple request, and you call the customer service line. Once the general service rep hands you off, you're transferred to every department known to man.

Traditionally, banks relied on limited data sets, such as credit history and income, to evaluate an individual’s creditworthiness. By analyzing this vast amount of data, fintech companies can identify patterns and trends that traditional banks may overlook, allowing them to create a more comprehensive credit scoring model.

However, I quickly discovered that there’s too much brand risk for a trusted bank to take this type of lean startup approach. Venus quickly became the key to getting everything done, including getting us a new banking licence! People were extremely privacy-conscious in Hong Kong and banks were trusted.

What does it take to integrate Generative AI into the highly regulated world of banking? Featured Links: Follow Tariq on LinkedIn | Citi | ‘Six things Read more » The post How Citi is accelerating AI in banking – Tariq Maonah (SVP of Product and Engineering, Citi) appeared first on Mind the Product.

Between heavy increases in usage as well as staggering drops in economic activity, 2020 was a roller coaster for banks, insurance companies, budgeting apps, and everything in between.

Blockchain is responsible for facilitating tasks in regular lives, investing protocols that can bring passive returns compared to the savings arenas and conventional banking. Blockchain also offers banking services. When you transact in cryptocurrencies, there is no need for you to input your banking data or personal information.

Couldn’t find Bank of Queensland’s Open Banking API (are they in breach of APRA or ACCC regulations?) Of the financial institutions that have an API, many have done the bare minimum to implement open banking. Is this in the spirit of Open Banking? Carsales.com.au Coles didn’t have a public API, whereas Woolworths did.

“When ATMs were introduced in the late 1960s, businesses weren’t sure consumers would ever embrace a machine over a bank teller” Instead, consumers want chatbots that respect their time and lead them to a desired outcome as quickly as possible. Just not in the way many chatbot makers envisioned it initially, eg.

Consumers used Finance apps for the same standard purposes, although DAU spiked as people used mobile as their primary access point to banks and finance management. Banking (banks and credit unions), and Insurance (auto, home, life, renters, pets, etc.). Finance brands were generally spared by the marketplace shakeup of 2020.

Now imagine the same scenario but this time, rather than a machine, you’re inside the bank speaking to a human cashier. In the Kano model, the surprise touches that users enjoy are called “delighters” For example, imagine a staff member handing a free lollipop to your child to keep them happy while you queue at the bank.

Ideal for businesses with weekly usage patterns (e.g., e-learning, businesstools). Monthly Active Users (MAU): Users engaged within a month. Relevant for services with less frequent interaction (e.g., DAU, WAU and MAU. Image by gainsight. Benchmarking examples Social media (e.g., Streaming services (e.g.,

The first sign that the thieves were on the move came when Tristan, CEO of a startup accelerator, was contacted by his bank, Monzo , through their app. Unfortunately, Tristan still had to handle charges on cards from two other banks. Using customer support to drive loyalty, engagement and revenue. 1 obstacle for these executives.

Meet the Continuous Discovery Champion, Teeba Teeba’s career so far has included four years in non-product roles, four years as a business owner, and four years working in fintech/banking product roles. Meet our continuous discovery champion, Teeba Alkhudairi. Teeba recently joined Lightspeed Commerce as a Senior Product Manager.

I call this type of trust-building process in relationships a “trust bank account.” Relationships are like bank accounts because you make deposits and withdrawals. However, like real bank accounts, trust cannot be built quickly. When you make continual deposits, your relationships become more fulfilling, happy and productive.

We organize all of the trending information in your field so you don't have to. Join 96,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content